Financial markets are now plunging following news that China has retaliated against the US over the tariffs announced by Donald Trump on Wednesday night.

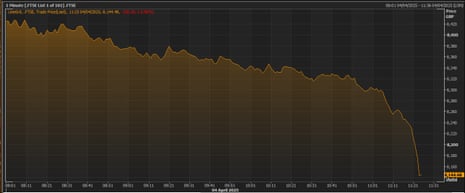

In London, the FTSE 100 has now shed 313 points, or 3.7%, since the start of trading to 8173 points. That would be its biggest one-day decline since March 2023.

As this chart shows, the selloff has intensified in the last few minutes:

The selloff intensified after China’s finance ministry said it will impose additional tariffs of 34% on all U.S. goods from April 10 as a countermeasure to sweeping tariffs imposed by the US.

China’s State Council Tariff Commission said in a statement:

“This practice of the US is not in line with international trade rules, seriously undermines China’s legitimate rights and interests, and is a typical unilateral bullying practice,”

Banks continue to lead the sell-off in London. Barclays are now down 10% today. with NatWest down 9.5%.

Rolls-Royce, the jet engine manufacturer and services, were briefly down 12%.

Fears of a global economic slowdown are hitting miners; Glencore are off 8.7%.

The US added 228,000 jobs in March, far more than expected, as the US economy shook off the blow from the Trump administration’s deep cuts to federal workers.

The figure was up from an adjusted 117,000 jobs added in February. Unemployment rose slightly to 4.2%.

Economists anticipated 140,000 jobs would be added in March 2025, a slight decrease from February and a continued decline from the monthly average of 167,000 jobs over the past 12 months. Payroll firm ADP reported 155,000 jobs were added in the private sector for March 2025.

Just in: the US economy added more jobs than expected last month.

Total nonfarm payroll employment rose by 228,000 in March, well ahead of forecasts for 135,000 new jobs last month.

The U.S. Bureau of Labor Statistics reports that there were job gains in health care, in social assistance, and in transportation and warehousing.

But federal government employment declined by 4,000 in March, following a loss of 11,000 jobs in February. (this does not count people on severance pay, though, so may not capture the impact of cuts driven by Elon Musk’s DOGE department).

The sight of China striking back against the US in Donald Trump’s trade war has driven global stock markets into ‘correction territory’ today.

MSCI’s All Country World Index, which covers companies across the global economy, is down over 1% today, after Beijing announced 34% tariffs on US goods.

That means it is over 10% below its record high, Reuters reports, a fall generally classed as a ‘correction’.

There are some dramatic moves in the currency markets today.

The Australian dollar has dropped by 3.5% today against the US dollar, while the Mexican peso is down 2.5%.

Risk appetite has taken “another big hit” as China struck back with fresh tariffs of its own against the US today, reports Fawad Razaqzada, market analyst at City Index and FOREX.com.

Razaqzada explains:

The world’s second largest economy has just announced a sweeping 34% tariff on all US goods, effective 10 April, escalating trade tensions yet again. In response, stocks, crude oil, and Aussie dollar all plunged, while government bonds and haven currencies – Japanese yen and Swiss franc – soared, alongside a rebounding gold.

With all these market tumbling, one has to wonder where it will all end.

So far, risk appetite has been literally non-existent. But there is still lingering hope that there might be some deals that could be agreed on before the April 9 go-live date for US reciprocal tariffs. However, as we get closer to that date, it looks like the trade war is only intensifying with China – and soon to follow others – coming back with counter measures.

Downing Street has said Sir Keir Starmer will be engaging with international leaders over the weekend, following the eruption of the global trade war that Donald Trump began this week.

A Number 10 spokesman said.

“We’ll be engaging with international leaders over the weekend.

“The need for engagement with international leaders is clear. It is a changing, shifting global economic landscape.”

The wave of selling gripping European markets has wiped 5% off the value of the Stoxx 600 index (of Europe’s largest 600 companies) today.

That takes its weekly losses to over 7.6%, which would be the worst week since March 2020, when the Covid-19 pandemic triggered a market crash.

Nearly every share on the FTSE 100 index is down today.

The only risers are United Utilities and National Grid, classic defensive stocks (on the ground that people will still want water and electricity in an economic downturn), consumer goods maker Unilever, and tobacco firm Imperial Brands.

The FTSE 100 remains deep, deep in the red, down 329 points or 3.9% at 8146 points, a three-month low.

The markets are “rattled” today after China’s retaliation against the US escalated the tariff war, reports Susannah Streeter, head of money and markets at Hargreaves Lansdown:

“Another jolt of fear has shot through markets, as China’s threat of retaliation has materialised. The big concern as that this a sign of a sharp escalation of the tariff war, which will have major implications for the global economy. The stock shock has shown up in even sharper losses with European indices sinking deeper into the red. Brent crude has also dropped sharply as expectations of a big hit to global growth and energy demand ratchets up.

The UK may appear to have been dealt a better hand in this round of tariffs, but it’s so interlinked with global trade, it’s set to be slammed by the harsh winds blowing through the global economy.

These kinds of market moves can feel incredibly uncomfortable, but anyone who has lived through any market turmoil in the past knows how important it is to focus on your long-term investment horizons and ride out short-term storms.

The pound has weakened against the US dollar today, as panicky traders seek out safe-haven currencies such as the Japanese yen and the Swiss franc.

Sterling has lost almost a cent against the dollar to just over $1.30.